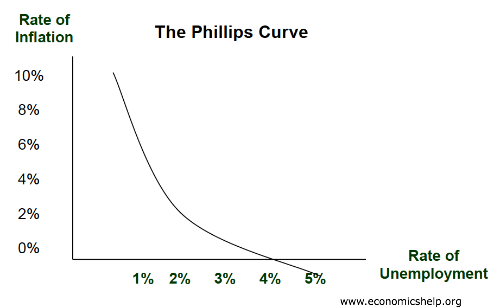

Phillips Curve

It is important to remember that the Phillips curve depicted above is simply an example. The actual Phillips curve for a country will vary depending upon the years that it aims to represent. While the Phillips curve is theoretically useful, however, it less practically helpful. The equation only holds in the short term. In the long run, unemployment always returns to the natural rate of unemployment, making cyclical unemployment zero and inflation equal to expected inflation.

In fact, the Phillips curve is not even theoretically perfect. In fact, there are many problems with it if it is taken as denoting anything more than a general relationship between unemployment and inflation. In particular, the Phillips curve does a terrible job of explaining the relationship between inflation and unemployment from 1970 to 1984. Inflation in these years was much higher than would have been expected given the unemployment for these years.

Such a situation of high inflation and high unemployment is called stagflation. The phenomenon of stagflation is somewhat of a mystery, though many economists believe that it results from changes in the error term of the previously stated Phillips curve equation. These errors can include things like energy cost increases and food price increases. But no matter its source, stagflation of the 1970's and early 1980's seems to refute the general applicability of the Phillips curve.

The Phillips curve must not be looked at as an exact set of points that the economy can reach and then remain at in equilibrium. Instead, the curve describes a historical picture of where the inflation rate has tended to be in relation to the unemployment rate. When the relationship is understood in this fashion, it becomes evident that the Phillips curve is useful not as a means of picking an unemployment and inflation rate pair, but rather as a means of understanding how unemployment and inflation might move given historical data.

No comments:

Post a Comment