Tuesday, February 26, 2013

Trade Off antara Efisiensi dan Equity(keadilan)

Dalam sektor publik terdapat konsep 3E yakni Ekonomi, Efisiensi, dan Efektivitas. 3E tersebut perlu diperluas dengan E yang ke empat yaitu Equity (keadilan).Dalam setiap penyelenggaraan Pemerintahan, khususnya negara yang menganut konsep Welfare State seperti Indonesia, pasti mengutamakan segi keadilan dan efisien. akan tetapi pada dasarnya kedua sifat ini akan mengalami trade off antara keduanya. trade off ini merupakan suatu hal pelik yang pasti terjadi dalam setiap penyelenggaraan pemerintahan.

Sebelum melanjutkan pembahasan pada trade antara efisiensi dan equity(keadilan), ada baiknya terlebih dalu kita membahas pengertian dari efisiensi dan equity(keadilan)

Efisiensi (efficiency) menurut kamus besar bahasa Indonesia yaitu tepat atau sesuai untuk mengerjakan (menghasilkan) sesuatu (dengan tidak membuang-buang waktu, tenaga, biaya), mampu menjalankan tugas dengan tepat dan cermat, berdaya guna, bertepat guna.

Sedangkan menurut definisi yang lain efisiensi adalah penggunaan sumber daya secara minimum guna pencapaian hasil yang optimum. Efisiensi menganggap bahwa tujuan-tujuan yang benar telah ditentukan dan berusaha untuk mencari cara-cara yang paling baik untuk mencapai tujuan-tujuan tersebut. Efisiensi hanya dapat dievaluasi dengan penilaian-penilaian relatif, membandingkan antara masukan dan keluaran yang diterima.terdapat 4 kondisi yang dapat digolongkan sebagai efisien :

a. Menghasilkan output yang lebih besar dengan menggunakan input tertentu.

b. Menghasilkan output tetap untuk input yang lebih rendah dari yang seharusnya.

c. Menghasilkan produksi yang lebih besar dari penggunaan sumber dayanya.

d. Mencapai hasil dengan biaya serendah mungkin.

Sedangkan pengertian equity sendiri menurut Kamus Besar Bahasa Indonesia, kata adil berarti tidak berat sebelah atau tidak memihak atau sewenang-wenang, sehingga keadilan mengandung pengertian sebagai suatu hal yang tidak berat sebelah atau tidak memihak atau sewenang-wenang

Menurut Frans Magnis Suseno dalam bukunya Etika Politik menyatakan bahwa keadilan sebagai suatu keadaan di mana orang dalam situasi yang sama diperlakukan secara sama.

Sedangkan menurut Aristoteles dalam tulisannya Retorica membedakan keadilan dalam dua macam :

a. Keadilan distributif atau justitia distributiva;

suatu keadilan yang memberikan kepada setiap orang didasarkan atas jasa-jasanya atau pembagian menurut haknya masing-masing. Keadilan distributif berperan dalam hubungan antara masyarakat dengan perorangan.

b. Keadilan kumulatif atau justitia cummulativa;

Suatu keadilan yang diterima oleh masing-masing anggota tanpa mempedulikan jasa masing-masing. Keadilan ini didasarkan pada transaksi baik yang sukarela atau tidak. Keadilan ini terjadi pada lapangan hukum perdata, misalnya dalam perjanjian tukar-menukar.

Terdapat dua masalah yang ditimbulkan dari trade off ini yaitu, untuk menurunkan ketidakadilan, seberapa besar efisiensi yang dikorbankan dan adanya ketidaksepakatan mengenai nilai relatif yang harus diberikan atas penurunan nilai ketidakadilan dibandingkan nilai efisiensi.

Sebagian berpendapat bahwa keadilan adalah masalah utama yang ada di masyarakat sehingga untuk memaksimalkannya harus mengorbankan efisiensi, begitu pula sebaliknya pandangan orang yang menyatakan bahwa efisiensi adalah masalah utama. Inilah mengapa antara efisiensi dan keadilan tidak bisa berjala bersama, harus ada salah satu yang dikorbankan.

Efisiensi terjadi ketika kondisi kesejahteraan tidak dapat ditingkatkan lagi tanpa mengorbankan tingkat kesejahteraan pihak lain (Pareto). Kalau dalam suatu komunitas ada A (50), B (100), dan C (1000) dengan angka di dalam kurung mewakili tingkat kesejahteraan hipotetis, maka menaikkan kesejahteraan A tanpa mengorbankan kesejahteraan B atau C adalah kondisi dimana terjadi perbaikan efisiensi (Pareto improvement); tetapi jika untuk menaikkan tingkat kesejahteraan salah satu anggota harus menurunkan kesejahteraan anggota lain, maka kondisi awal ini sudah menunjukkan Pareto efficient.

Di lain sisi,keadilan adalah suatu istilah yang batasannya tidak tegas dan sangat relatif. Adil bagi C belum tentu dianggap adil bagi A atau B. Kita tidak bisa memuaskan semua pihak sekaligus. Subsidi BBM secara massal tidak efisien karena memicu over-consumption dan dinikmati golongan yang tidak seharusnya menerima subsidi. Tetapi dengan struktur ekonomi dan bisnis kita yang memang tidak efisien, menghilangkan subsidi sekaligus akan membuat kehidupan lapisan miskin semakin menderita. Di sini kita lihat ada trade-off antara efficiency dan equity. Saya tidak hendak membahas mana yang terbaik tetapi hanya ingin menunjukkan bahwa dalam hampir semua hal efficiency itu bekerja berlawanan arah dengan equity.

Dengan demikian dapat ditarik kesimpulan bahwa pada kenyataannya, efisiensi dan keadilan sering sekali tidak dapat sejalan. Untuk mencapai efisiensi maka harus mengorbankan keadilan, begitu pula sebaliknya. Kaedilan dapat dicapai tetapi konsekuensinya adalah menurunnya efisiensi. First fundamental theorem of welfare economics menyatakan bahwa ekuilibrium yang kompetitif dapat mencapai pareto optimum dalam pasar yang sempurna. Dalam kenyataannya, terjadi kegagalan pasar (market failure), sehingga lahirlah second fundamental theorem of welfare economics yang menyatakan bahwa dalam konteks terjadi kegagalan pasar, ekuilibrium yang kompetitif dan memiliki properti pareto yang optimal dapat dicapai melalui lumpsum transfer. Hal inilah yang kemudian menjadi dasar intervensi pemerintah untuk mengatasi trade-off antara efisiensi dan pemerataan melalui kebijakan redistribusi dalam bentuk pajak, subsidi, dan pengeluaran publik pemerintah.

Saturday, February 23, 2013

Short Run Trade Off Between Inflation and Unemployment

In the short run, an increase in the quantity of money stimulates spending, which raises both prices and production. The increase in production requires more hiring, which reduces unemployment. Thus, in the short run, an increase in inflation tends to reduce unemployment, causing a trade-off between inflation and unemployment. The trade-off is temporary but can last for a year or two. Understanding this trade-off is important for understanding the fluctuations in economic activity known as the business cycle. In the short run, policy makers may be able to affect the mix of inflation and unemployment by changing government spending, taxes, and the quantity of money.

Although a higher level of prices is, in the long run, the primary effect of increasing the quantity of money, the short-run story is more complex and controversial. Most economists describe the short-run effects of monetary injections as follows:

This line of reasoning leads to one final economy-wide trade-off: a short-run tradeoff between inflation and unemployment. Although some economists still question these ideas, most accept that society faces a short-run trade-off between inflation and unemployment. This simply means that, over a period of a year or two, many economic policies push inflation and unemployment in opposite directions. Policymakers face this trade-off regardless of whether inflation and unemployment both start out at high levels (as they were in the early 1980s), at low levels (as they were in the late 1990s), or someplace in between. This short-run trade-off plays a key role in the analysis of the business cycle—the irregular and largely unpredictable fluctuations in economic activity, as measured by the production of goods and services or the number of people employed.

Policymakers can exploit the short-run trade-off between inflation and unemployment using various policy instruments. By changing the amount that the government spends, the amount it taxes, and the amount of money it prints, policymakers can influence the overall demand for goods and services. Changes in demand in turn influence the combination of inflation and unemployment that the economy experiences in the short-run. Because these instruments of economic policy are potentially so powerful, how policymakers should use these instruments to control the economy, if at all, is a subject of continuing debate.

Although a higher level of prices is, in the long run, the primary effect of increasing the quantity of money, the short-run story is more complex and controversial. Most economists describe the short-run effects of monetary injections as follows:

- Increasing the amount of money in the economy stimulates the overall level of spending and thus the demand for goods and services.

- Higher demand may over time cause firms to raise their prices, but in the meantime, it also encourages them to hire more workers and produce a larger quantity of goods and services.

- More hiring means lower unemployment.

This line of reasoning leads to one final economy-wide trade-off: a short-run tradeoff between inflation and unemployment. Although some economists still question these ideas, most accept that society faces a short-run trade-off between inflation and unemployment. This simply means that, over a period of a year or two, many economic policies push inflation and unemployment in opposite directions. Policymakers face this trade-off regardless of whether inflation and unemployment both start out at high levels (as they were in the early 1980s), at low levels (as they were in the late 1990s), or someplace in between. This short-run trade-off plays a key role in the analysis of the business cycle—the irregular and largely unpredictable fluctuations in economic activity, as measured by the production of goods and services or the number of people employed.

Policymakers can exploit the short-run trade-off between inflation and unemployment using various policy instruments. By changing the amount that the government spends, the amount it taxes, and the amount of money it prints, policymakers can influence the overall demand for goods and services. Changes in demand in turn influence the combination of inflation and unemployment that the economy experiences in the short-run. Because these instruments of economic policy are potentially so powerful, how policymakers should use these instruments to control the economy, if at all, is a subject of continuing debate.

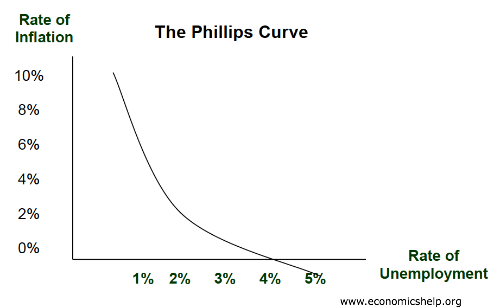

The trade off between inflation and unemployment

Okun's Law describes a clear relationship between unemployment and national output, in which lowered unemployment results in higher national output. Such a relationship makes intuitive sense: as more people in a nation work it seems only right that the output of the nation should increase. Building on Okun's law, another economist, A. W. Phillips, discovered a relationship between unemployment and inflation. The chain of basic ideas behind this belief follows: as more people work the national output increases, causing wages to increase, causing consumers to have more money and to spend more, resulting in consumers demanding more goods and services, finally causing the prices of goods and services to increase. In other words, Phillips showed that unemployment and inflation shared an inverse relationship: inflation rose as unemployment fell, and inflation fell as unemployment rose.

Phillips Curve

It is important to remember that the Phillips curve depicted above is simply an example. The actual Phillips curve for a country will vary depending upon the years that it aims to represent. While the Phillips curve is theoretically useful, however, it less practically helpful. The equation only holds in the short term. In the long run, unemployment always returns to the natural rate of unemployment, making cyclical unemployment zero and inflation equal to expected inflation.

In fact, the Phillips curve is not even theoretically perfect. In fact, there are many problems with it if it is taken as denoting anything more than a general relationship between unemployment and inflation. In particular, the Phillips curve does a terrible job of explaining the relationship between inflation and unemployment from 1970 to 1984. Inflation in these years was much higher than would have been expected given the unemployment for these years.

Such a situation of high inflation and high unemployment is called stagflation. The phenomenon of stagflation is somewhat of a mystery, though many economists believe that it results from changes in the error term of the previously stated Phillips curve equation. These errors can include things like energy cost increases and food price increases. But no matter its source, stagflation of the 1970's and early 1980's seems to refute the general applicability of the Phillips curve.

The Phillips curve must not be looked at as an exact set of points that the economy can reach and then remain at in equilibrium. Instead, the curve describes a historical picture of where the inflation rate has tended to be in relation to the unemployment rate. When the relationship is understood in this fashion, it becomes evident that the Phillips curve is useful not as a means of picking an unemployment and inflation rate pair, but rather as a means of understanding how unemployment and inflation might move given historical data.

Phillips Curve

It is important to remember that the Phillips curve depicted above is simply an example. The actual Phillips curve for a country will vary depending upon the years that it aims to represent. While the Phillips curve is theoretically useful, however, it less practically helpful. The equation only holds in the short term. In the long run, unemployment always returns to the natural rate of unemployment, making cyclical unemployment zero and inflation equal to expected inflation.

In fact, the Phillips curve is not even theoretically perfect. In fact, there are many problems with it if it is taken as denoting anything more than a general relationship between unemployment and inflation. In particular, the Phillips curve does a terrible job of explaining the relationship between inflation and unemployment from 1970 to 1984. Inflation in these years was much higher than would have been expected given the unemployment for these years.

Such a situation of high inflation and high unemployment is called stagflation. The phenomenon of stagflation is somewhat of a mystery, though many economists believe that it results from changes in the error term of the previously stated Phillips curve equation. These errors can include things like energy cost increases and food price increases. But no matter its source, stagflation of the 1970's and early 1980's seems to refute the general applicability of the Phillips curve.

The Phillips curve must not be looked at as an exact set of points that the economy can reach and then remain at in equilibrium. Instead, the curve describes a historical picture of where the inflation rate has tended to be in relation to the unemployment rate. When the relationship is understood in this fashion, it becomes evident that the Phillips curve is useful not as a means of picking an unemployment and inflation rate pair, but rather as a means of understanding how unemployment and inflation might move given historical data.

Trade Off

whats's the meaning of trade off ?

Trade-off is a situation that involves losing one quality or aspect of something in return for gaining another quality or aspect. It often implies a decision to be made with full comprehension of both the upside and downside of a particular choice; the term is also used in an evolutionary context, in which case the selection process acts as the "decision-maker".

In another description of trade off is when choices are made (collectively or by an individual) to accept having less of one thing in order to get more of something else

examples of trade off

when one is allocating (limited) funds, the trade-off usually involves reduced spending for some purposes in order to be able to spend more for other more urgent purposes. However, the concept does not apply only (or even primarily) to decisions involving money. A student faced with the choice of spending Saturday studying for a Political Economy exam or shopping at The Mall makes a trade-off of shopping time for study time in deciding how many hours to study and how many to spend shopping.

In economics the term is expressed as opportunity cost, referring to the most preferred alternative given up. A trade-off, then, involves a sacrifice that must be made to obtain a certain product, rather than other products that can be made using the same required resources. For a person going to a basketball game, its opportunity cost is the money and time expended, say that would have been spent watching a particular television program.

Society also makes trade-offs, such as, for example, between its need for a more plentiful supply of energy and its need to prevent excessive deterioration of the environment caused by energy production technologies. Evaluating trade-offs, when done carefully and systematically, involves comparing the opportunity costs and benefits of each of the available alternatives with each other. Most choices (and thus most trade-offs) are not all-or-nothing decisions; rather they typically involve small changes at the margin, a little more of this at the cost of a little less of that. Consumers continuously practice marginalism and make trade-offs as they consider whether to buy one more unit or one unit less of a good or service in their efforts to obtain a mix of goods and services that afford them the greatest satisfaction for their available buying power. Producers must constantly be deciding and reevaluating their trade-offs in choosing whether to produce somewhat more or somewhat less of a particular product, whether to add a few more workers or lay a few off, whether to invest in more plant and equipment or whether to close down some of existing capacity, and so on, in their efforts to maximize profits.

Trade-off is a situation that involves losing one quality or aspect of something in return for gaining another quality or aspect. It often implies a decision to be made with full comprehension of both the upside and downside of a particular choice; the term is also used in an evolutionary context, in which case the selection process acts as the "decision-maker".

In another description of trade off is when choices are made (collectively or by an individual) to accept having less of one thing in order to get more of something else

examples of trade off

when one is allocating (limited) funds, the trade-off usually involves reduced spending for some purposes in order to be able to spend more for other more urgent purposes. However, the concept does not apply only (or even primarily) to decisions involving money. A student faced with the choice of spending Saturday studying for a Political Economy exam or shopping at The Mall makes a trade-off of shopping time for study time in deciding how many hours to study and how many to spend shopping.

In economics the term is expressed as opportunity cost, referring to the most preferred alternative given up. A trade-off, then, involves a sacrifice that must be made to obtain a certain product, rather than other products that can be made using the same required resources. For a person going to a basketball game, its opportunity cost is the money and time expended, say that would have been spent watching a particular television program.

Society also makes trade-offs, such as, for example, between its need for a more plentiful supply of energy and its need to prevent excessive deterioration of the environment caused by energy production technologies. Evaluating trade-offs, when done carefully and systematically, involves comparing the opportunity costs and benefits of each of the available alternatives with each other. Most choices (and thus most trade-offs) are not all-or-nothing decisions; rather they typically involve small changes at the margin, a little more of this at the cost of a little less of that. Consumers continuously practice marginalism and make trade-offs as they consider whether to buy one more unit or one unit less of a good or service in their efforts to obtain a mix of goods and services that afford them the greatest satisfaction for their available buying power. Producers must constantly be deciding and reevaluating their trade-offs in choosing whether to produce somewhat more or somewhat less of a particular product, whether to add a few more workers or lay a few off, whether to invest in more plant and equipment or whether to close down some of existing capacity, and so on, in their efforts to maximize profits.

Monday, February 18, 2013

Public Sector Auditing

Public Sector Auditing is an activity directed towards entities that provide services and supply of goods whose financing comes from tax revenues and other revenues for the purpose of comparing the conditions found and the criteria set. A public sector audit refers to audits covering the government, healthcare, education, charities and other public non-for-profit organisations. There are accounting firms that specialise in such public sector audits, not only providing general auditing services, but other advice, such as how effectively these organisations can make use of taxpayer money or how best to manage their financial assets. However, unlike audits for private organisations, an auditor, auditing a public organisation may also go further to assess whether the public organisation is meeting its mission or objectives.

In Indonesia, public sector auditing regulated in 'UU no.15 tahun 2004' and called state finacial audit.

In Indonesia, public sector auditing regulated in 'UU no.15 tahun 2004' and called state finacial audit.

Aparat Pengawas Internal Pemerintah

Aparat Pengawas Internal Pemerintah adalah unit organisasi di lingkungan Pemerintah Pusat, Pemerintah Daerah, Kementerian Negara, Lembaga Negara dan Lembaga Pemerintah Non Departemen yang mempunyai tugas dan fungsi melakukan pengawasan dalam lingkup kewenangannya. Itjen Kemenkeu merupakan APIP untuk melakukan pengawasan pada unit-unit di lingkungan Kementerian Keuangan

Pengendalian intern merupakan proses integral pada tindakan dan kegiatan yang dilaksanakan secara terus menerus oleh pimpinan dan seluruh pegawai untuk memberikan keyakinan memadai atas tercapainya tujuan organisasi melalui kegiatan yang efektif dan efisien, keandalan pelaporan keuangan, pengamanan aset negara, dan ketaatan terhadap peraturan perundang-undangan yang berlaku.

Sistem Pengendalian Intern Pemerintah (SPIP) adalah proses yang integral pada tindakan dan kegiatan yang dilakukan secara terus menerus oleh pimpinan dan seluruh pegawai untuk memberikan keyakinan memadai atas tercapainya tujuan organisasi melalui kegiatan yang efektif dan efisien, keandalan pelaporan keuangan, pengamanan aset negara, dan ketaatan terhadap peraturan perundang-undangan yang diselenggarakan secara menyeluruh di lingkungan pemerintah pusat dan pemerintah daerah.

Dalam sejarah pengawasan internal pemerintah sampai saat ini terdapat beberapa lembaga yang mengemban tugas pengawasan internal tersebut, yakni :

Sejarah panjang dari audit kinerja sektor pemerintah yang ada di Indonesia ini dimulai sejak munculnya lembaga pengawasan sebelum era kemerdekaan. Dimulai dengan munculnya Besluit Nomor 44 tanggal 31 Oktober 1936 secara eksplisit ditetapkan bahwa Djawatan Akuntan Negara (Regering Accountantsdienst) bertugas melakukan penelitian terhadap pembukuan dari berbagai perusahaan negara dan jawatan tertentu, sehingga dapat dikatakan aparat pengawasan pertama di Indonesia adalah Djawatan Akuntan Negara (DAN). Secara struktural DAN yang bertugas mengawasi pengelolaan perusahaan negara berada di bawah Thesauri Jenderal pada Kementerian Keuangan.

Kemudian dengan Peraturan Presiden Nomor 9 Tahun 1961 tentang Instruksi bagi Kepala Djawatan Akuntan Negara (DAN), kedudukan DAN dilepas dari Thesauri Jenderal dan ditingkatkan kedudukannya langsung di bawah Menteri Keuangan. DAN merupakan alat pemerintah yang bertugas melakukan semua pekerjaan akuntan bagi pemerintah atas semua departemen, jawatan, dan instansi di bawah kekuasaannya. Sementara itu fungsi pengawasan anggaran dilaksanakan oleh Thesauri Jenderal. Selanjutnya dengan Keputusan Presiden Nomor 239 Tahun 1966 dibentuklah Direktorat Djendral Pengawasan Keuangan Negara (DDPKN) pada Departemen Keuangan. Tugas DDPKN (kemudian dikenal sebagai DJPKN) meliputi pengawasan anggaran dan pengawasan badan usaha/jawatan, yang semula menjadi tugas DAN dan Thesauri Jenderal.

DJPKN mempunyai tugas melaksanakan pengawasan seluruh pelaksanaan anggaran negara, anggaran daerah, dan badan usaha milik negara/daerah. Berdasarkan Keputusan Presiden Nomor 70 Tahun 1971 ini, khusus pada Departemen Keuangan, tugas Inspektorat Jendral dalam bidang pengawasan keuangan negara dilakukan oleh DJPKN.

Dengan diterbitkan Keputusan Presiden Nomor 31 Tahun 1983 tanggal 30 Mei 1983. DJPKN ditransformasikan menjadi BPKP, sebuah lembaga pemerintah non departemen (LPND) yang berada di bawah dan bertanggung jawab langsung kepada Presiden. Salah satu pertimbangan dikeluarkannya Keputusan Presiden Nomor 31 Tahun 1983 tentang BPKP adalah diperlukannya badan atau lembaga pengawasan yang dapat melaksanakan fungsinya secara leluasa tanpa mengalami kemungkinan hambatan dari unit organisasi pemerintah yang menjadi obyek pemeriksaannya. Keputusan Presiden Nomor 31 Tahun 1983 tersebut menunjukkan bahwa Pemerintah telah meletakkan struktur organisasi BPKP sesuai dengan proporsinya dalam konstelasi lembaga-lembaga Pemerintah yang ada. BPKP dengan kedudukannya yang terlepas dari semua departemen atau lembaga sudah barang tentu dapat melaksanakan fungsinya secara lebih baik dan obyektif.

BPK

Pasal 23 ayat (5) UUD Tahun 1945 menetapkan bahwa untuk memeriksa tanggung jawab tentang Keuangan Negara diadakan suatu Badan Pemeriksa Keuangan yang peraturannya ditetapkan dengan Undang-Undang. Hasil pemeriksaan itu disampaikan kepada Dewan Perwakilan Rakyat. Berdasarkan amanat UUD Tahun 1945 tersebut telah dikeluarkan Surat Penetapan Pemerintah No.11/OEM tanggal 28 Desember 1946 tentang pembentukan Badan Pemeriksa Keuangan, pada tanggal 1 Januari 1947 yang berkedudukan sementara dikota Magelang. Untuk memulai tugasnya, Badan Pemeriksa Keuangan dengan suratnya tanggal 12 April 1947 No.94-1 telah mengumumkan kepada semua instansi di Wilayah Republik Indonesia mengenai tugas dan kewajibannya dalam memeriksa tanggung jawab tentang Keuangan Negara, untuk sementara masih menggunakan peraturan perundang-undangan yang dulu berlaku bagi pelaksanaan tugas Algemene Rekenkamer (Badan Pemeriksa Keuangan Hindia Belanda), yaitu ICW dan IAR.

Dengan terbentuknya Negara Kesatuan Republik Indonesia Serikat (RIS) berdasarkan Piagam Konstitusi RIS tanggal 14 Desember 1949, maka dibentuk Dewan Pengawas Keuangan yang merupakan salah satu alat perlengkapan negara RIS. Dengan kembalinya bentuk Negara menjadi Negara Kesatuan Republik Indonesia padatanggal 17 Agustus 1950, maka Dewan Pengawas Keuangan RIS yang berada di Bogor sejak tanggal 1 Oktober 1950 digabung dengan Badan Pemeriksa Keuangan berdasarkan UUDS 1950 dan berkedudukan di Bogor.

Pada Tanggal 5 Juli 1959 dikeluarkan Dekrit Presiden RI yang menyatakan berlakunya kembali UUD Tahun 1945. Dengan demikian Dewan Pengawas Keuangan berdasarkan UUD 1950 kembali menjadi Badan Pemeriksa Keuangan berdasarkan Pasal 23 (5) UUD Tahun 1945.

Inspektorat Jenderal

Dalam rangka pembenahan aparatur pemerintah pada awal berdirinya Orde Baru tahun 1966, berdasarkan Keputusan Presidium Kabinet Ampera Nomor 15/U/Kep/8/1966 tanggal 31 Agustus 1966 ditetapkan antara lain kedudukan, tugas pokok dan fungsi Inspektorat Jenderal Departemen. Pembentukan Institusi Inspektorat Jenderal pada suatu Departemen pada saat itu dilakukan sesuai kebutuhan. Dengan Keputusan Presidium Kabinet Ampera Nomor 38/U/Kep/9/1966 tanggal 21 September 1966 dibentuk Inspektorat Jenderal pada delapan departemen termasuk Departemen Keuangan dan sekaligus mengangkat H.A.Pandelaki sebagai Pejabat Inspektur Jenderal Departemen Keuangan.

Masih dalam Kabinet Ampera, dengan Keputusan Menteri Keuangan Nomor 133/Men.Keu/1967 tanggal 20 Juli 1967 ditetapkan (sambil menunggu pengesahan dari Presidium Kabinet Ampera), pembentukan Badan Alat Pelaksana Utama Pengawasan Departemen Keuangan yaitu Inspektorat Jenderal Departemen Keuangan dan mengangkat Drs. Gandhi sebagai Pejabat Inspektur Jenderal Departemen Keuangan.

Memasuki masa Kabinet Pembangunan dengan Rencana Pembangunan Lima Tahunnya (Repelita), upaya penyempurnaan aparatur pemerintah baik tingkat pusat maupun di tingkat daerah terus dilanjutkan. Pada awal pelaksanaan Repelita II tepatnya tanggal 26 Agustus 1974, terbit Keputusan Presiden Nomor 44 tahun 1974 tentang susunan Organisasi Departemen. Sebagai pelaksanaan Keputusan Presiden Nomor 44 dan 45 tahun 1974 di atas, diterbitkanlah Keputusan Menteri Keuangan Nomor 405/KMK/6/1975 tanggal 16 April 1975 tentang Susunan Orgasnisasi dan Tata Kerja Departemen Keuangan, di mana dalam Pasal 189 Keputusan Menteri Keuangan tersebut menetapkan susunan Organisasi Inspektorat Jenderal Departemen Keuangan. Kemudian di masa-masa berikutnya, susunana organisasi Inspektorat Jenderal senantiasa mengalami perkembangan dan penyempurnaan.

Terakhir berdasarkan Keputusan Menteri Keuangan Nomor 184/KMK.01/2010 maka susunan organisasi Inspektorat Jenderal Departemen Keuangan semakin dikukuhkan menjadi sebagai berikut:

1. Sekretariat Inspektorat Jenderal

2. Inspektorat I

3. Inspektorat II

4. Inspektorat III

5. Inspektorat IV

6. Inspektorat V

7. Inspektorat VI

8. Inspektorat VII

9. Inspektorat Bidang Investigasi

Dalam sejarah pengawasan internal pemerintah sampai saat ini terdapat beberapa lembaga yang mengemban tugas pengawasan internal tersebut, yakni :

DAN, DJPKN, dan BPKP

Djawatan Akuntan Negara (Governement Accountantsdienst)

Besluit Nomor 44 tanggal 31 Oktober 1936

Direktorat Djendral Pengawasan Keuangan Negara (DDPKN/DJPKN) pada Departemen Keuangan

Keputusan Presiden Nomor 239 Tahun 1966

BPKP

Keputusan Presiden Nomor 31 Tahun 1983 tanggal 30 Mei 1983

Sejarah panjang dari audit kinerja sektor pemerintah yang ada di Indonesia ini dimulai sejak munculnya lembaga pengawasan sebelum era kemerdekaan. Dimulai dengan munculnya Besluit Nomor 44 tanggal 31 Oktober 1936 secara eksplisit ditetapkan bahwa Djawatan Akuntan Negara (Regering Accountantsdienst) bertugas melakukan penelitian terhadap pembukuan dari berbagai perusahaan negara dan jawatan tertentu, sehingga dapat dikatakan aparat pengawasan pertama di Indonesia adalah Djawatan Akuntan Negara (DAN). Secara struktural DAN yang bertugas mengawasi pengelolaan perusahaan negara berada di bawah Thesauri Jenderal pada Kementerian Keuangan.

Kemudian dengan Peraturan Presiden Nomor 9 Tahun 1961 tentang Instruksi bagi Kepala Djawatan Akuntan Negara (DAN), kedudukan DAN dilepas dari Thesauri Jenderal dan ditingkatkan kedudukannya langsung di bawah Menteri Keuangan. DAN merupakan alat pemerintah yang bertugas melakukan semua pekerjaan akuntan bagi pemerintah atas semua departemen, jawatan, dan instansi di bawah kekuasaannya. Sementara itu fungsi pengawasan anggaran dilaksanakan oleh Thesauri Jenderal. Selanjutnya dengan Keputusan Presiden Nomor 239 Tahun 1966 dibentuklah Direktorat Djendral Pengawasan Keuangan Negara (DDPKN) pada Departemen Keuangan. Tugas DDPKN (kemudian dikenal sebagai DJPKN) meliputi pengawasan anggaran dan pengawasan badan usaha/jawatan, yang semula menjadi tugas DAN dan Thesauri Jenderal.

DJPKN mempunyai tugas melaksanakan pengawasan seluruh pelaksanaan anggaran negara, anggaran daerah, dan badan usaha milik negara/daerah. Berdasarkan Keputusan Presiden Nomor 70 Tahun 1971 ini, khusus pada Departemen Keuangan, tugas Inspektorat Jendral dalam bidang pengawasan keuangan negara dilakukan oleh DJPKN.

Dengan diterbitkan Keputusan Presiden Nomor 31 Tahun 1983 tanggal 30 Mei 1983. DJPKN ditransformasikan menjadi BPKP, sebuah lembaga pemerintah non departemen (LPND) yang berada di bawah dan bertanggung jawab langsung kepada Presiden. Salah satu pertimbangan dikeluarkannya Keputusan Presiden Nomor 31 Tahun 1983 tentang BPKP adalah diperlukannya badan atau lembaga pengawasan yang dapat melaksanakan fungsinya secara leluasa tanpa mengalami kemungkinan hambatan dari unit organisasi pemerintah yang menjadi obyek pemeriksaannya. Keputusan Presiden Nomor 31 Tahun 1983 tersebut menunjukkan bahwa Pemerintah telah meletakkan struktur organisasi BPKP sesuai dengan proporsinya dalam konstelasi lembaga-lembaga Pemerintah yang ada. BPKP dengan kedudukannya yang terlepas dari semua departemen atau lembaga sudah barang tentu dapat melaksanakan fungsinya secara lebih baik dan obyektif.

BPK

Pasal 23 ayat (5) UUD Tahun 1945 menetapkan bahwa untuk memeriksa tanggung jawab tentang Keuangan Negara diadakan suatu Badan Pemeriksa Keuangan yang peraturannya ditetapkan dengan Undang-Undang. Hasil pemeriksaan itu disampaikan kepada Dewan Perwakilan Rakyat. Berdasarkan amanat UUD Tahun 1945 tersebut telah dikeluarkan Surat Penetapan Pemerintah No.11/OEM tanggal 28 Desember 1946 tentang pembentukan Badan Pemeriksa Keuangan, pada tanggal 1 Januari 1947 yang berkedudukan sementara dikota Magelang. Untuk memulai tugasnya, Badan Pemeriksa Keuangan dengan suratnya tanggal 12 April 1947 No.94-1 telah mengumumkan kepada semua instansi di Wilayah Republik Indonesia mengenai tugas dan kewajibannya dalam memeriksa tanggung jawab tentang Keuangan Negara, untuk sementara masih menggunakan peraturan perundang-undangan yang dulu berlaku bagi pelaksanaan tugas Algemene Rekenkamer (Badan Pemeriksa Keuangan Hindia Belanda), yaitu ICW dan IAR.

Dengan terbentuknya Negara Kesatuan Republik Indonesia Serikat (RIS) berdasarkan Piagam Konstitusi RIS tanggal 14 Desember 1949, maka dibentuk Dewan Pengawas Keuangan yang merupakan salah satu alat perlengkapan negara RIS. Dengan kembalinya bentuk Negara menjadi Negara Kesatuan Republik Indonesia padatanggal 17 Agustus 1950, maka Dewan Pengawas Keuangan RIS yang berada di Bogor sejak tanggal 1 Oktober 1950 digabung dengan Badan Pemeriksa Keuangan berdasarkan UUDS 1950 dan berkedudukan di Bogor.

Pada Tanggal 5 Juli 1959 dikeluarkan Dekrit Presiden RI yang menyatakan berlakunya kembali UUD Tahun 1945. Dengan demikian Dewan Pengawas Keuangan berdasarkan UUD 1950 kembali menjadi Badan Pemeriksa Keuangan berdasarkan Pasal 23 (5) UUD Tahun 1945.

Inspektorat Jenderal

Dalam rangka pembenahan aparatur pemerintah pada awal berdirinya Orde Baru tahun 1966, berdasarkan Keputusan Presidium Kabinet Ampera Nomor 15/U/Kep/8/1966 tanggal 31 Agustus 1966 ditetapkan antara lain kedudukan, tugas pokok dan fungsi Inspektorat Jenderal Departemen. Pembentukan Institusi Inspektorat Jenderal pada suatu Departemen pada saat itu dilakukan sesuai kebutuhan. Dengan Keputusan Presidium Kabinet Ampera Nomor 38/U/Kep/9/1966 tanggal 21 September 1966 dibentuk Inspektorat Jenderal pada delapan departemen termasuk Departemen Keuangan dan sekaligus mengangkat H.A.Pandelaki sebagai Pejabat Inspektur Jenderal Departemen Keuangan.

Masih dalam Kabinet Ampera, dengan Keputusan Menteri Keuangan Nomor 133/Men.Keu/1967 tanggal 20 Juli 1967 ditetapkan (sambil menunggu pengesahan dari Presidium Kabinet Ampera), pembentukan Badan Alat Pelaksana Utama Pengawasan Departemen Keuangan yaitu Inspektorat Jenderal Departemen Keuangan dan mengangkat Drs. Gandhi sebagai Pejabat Inspektur Jenderal Departemen Keuangan.

Memasuki masa Kabinet Pembangunan dengan Rencana Pembangunan Lima Tahunnya (Repelita), upaya penyempurnaan aparatur pemerintah baik tingkat pusat maupun di tingkat daerah terus dilanjutkan. Pada awal pelaksanaan Repelita II tepatnya tanggal 26 Agustus 1974, terbit Keputusan Presiden Nomor 44 tahun 1974 tentang susunan Organisasi Departemen. Sebagai pelaksanaan Keputusan Presiden Nomor 44 dan 45 tahun 1974 di atas, diterbitkanlah Keputusan Menteri Keuangan Nomor 405/KMK/6/1975 tanggal 16 April 1975 tentang Susunan Orgasnisasi dan Tata Kerja Departemen Keuangan, di mana dalam Pasal 189 Keputusan Menteri Keuangan tersebut menetapkan susunan Organisasi Inspektorat Jenderal Departemen Keuangan. Kemudian di masa-masa berikutnya, susunana organisasi Inspektorat Jenderal senantiasa mengalami perkembangan dan penyempurnaan.

Terakhir berdasarkan Keputusan Menteri Keuangan Nomor 184/KMK.01/2010 maka susunan organisasi Inspektorat Jenderal Departemen Keuangan semakin dikukuhkan menjadi sebagai berikut:

1. Sekretariat Inspektorat Jenderal

2. Inspektorat I

3. Inspektorat II

4. Inspektorat III

5. Inspektorat IV

6. Inspektorat V

7. Inspektorat VI

8. Inspektorat VII

9. Inspektorat Bidang Investigasi

Sunday, February 17, 2013

History of Public Sector Performance Audit in Indonesia

Performance audit first became known in Indonesia in the private sector through internal audit in foreign companies such as BPM, Stanvac, Shell, and Unilever. In the government sector, has pioneered DJPKN performance audits since the early 1970's, and began to be implemented programmatically in the 1980s.

Broadly, the historical development of public sector performance audits in Indonesia can be explained as follows:

- 1936

With 'besluit No. 44 dated October 31, 1936' explicitly stated that Djawatan Akuntan Negara (DAN) assigned to conduct research on the books of the various state enterprises and certain office. Thus, it can be said That the first APIP (aparat pengawas internal pemerintah/Internal government regulatory authorities) in Indonesia is Djawatan Akuntan Negara(DAN). Structurally DAN - which oversees the management of state-owned companies - are under the Ministry of Finance.

- 1959

With the Finance Minister Regulation No. 175/BDS/V dated December 19, 1959, Djawatan Akuntan Pajak (DAP) were formed in 1921 - also under the Ministry of Finance - combined with DAN.

- 1961

Furthermore, by Presidential Decree No. 9 of 1961 on the instructions for the Chief of Djawatan Akuntan Negara (DAN), DAN was removed from the position of General of Treasury and enhanced its position directly under the Ministry of Finance. DAN is a tool of the government in charge of doing all the work for government accountants for all departments, department and agencies under his control. Meanwhile, budget oversight function performed by Treasury General.

- 1963

By Presidential Decree No. 29 Year 1963 on State Finance Supervision, Supervision Affairs established the Department of Revenue, Finance and Control (read: Ministry of Finance). While in each of the Department of Financial Control Section was independently formed of the Finance Department is concerned. The working relationship between Affairs Oversight and Financial Control Section is coordinated.

- 1966

By Presidential Decree No. 239 of 1966 established Direktorat Djendral Pengawasan Keuangan Negara (DDPKN)/the State Financial Supervision Directorate generals in the Ministry of Finance. DDPKN Duties include oversight of the budget and oversight entity / department, which was originally the duty of DAN and Thesauri General.

- 1968

By Presidential Decree No. 26 Year 1968 on January 24, 1968 on State Financial Control repealed Presidential Decree No. 29 Year 1963. Presidential Decree No. 26 of 1968 applies retroactively to the date of 15 November 1966 the date of the establishment of DDPKN. based on this Presidential Decree, DDPKN consists of three directorates namely Direktorat Pengawasan Anggaran Negara (DPAN)/the Directorate of State Budget Monitoring, Direkorat Akuntan Negara (DAN)/Directorate of State Accountant, and Direktorat Tata Usaha Keuangan Negara (DTUKN)/the Directorate of State Finance Administration.

Based on Presidential Decree No. 26 of 1968 is also in each department / agency that controls the state budget section itself, held unit Financial Supervision under the leadership of Inspector General of the Department.

- 1971

By Presidential Decree Number 70 of 1971 on State Finance Monitoring Working Procedure, DDPKN (known then as DJPKN) split itself with the creation of several new directorates, Direktorat Pengawasan Perminyakan (DPP)/the Directorate of Petroleum Monitoring, Direktorak Perencanaan dan Analisa (DPA)/the Directorate of Planning and Analysis, Direktorat Pengawasan Internal (DPI)/Directorate of Internal Audit which later became Direktorat Pengawasan Kas Negara (DPKsN) the Directorate of Treasury, Direktorat Pembukuan Keuangan Negara DPbKN)/State Finance and Accounting Directorate. DJPKN has the tasks of control over the entire execution of the state budget, region budgets, and state-owned enterprises / regions. Based on Presidential Decree No. 70 Year 1971, specifically in the Financial Department, the task of the Inspectorate General of the state in the areas of financial control by DJPKN.

- 1983

Issued Presidential Decree No. 31 Year 1983 on May 30, 1983. DJPKN (Direktorat Jendral Pengawasan Keuangan Negara) transformed into BPKP (Badan Pengawas Keuangan dan Pembangunan), a non-departmental government agencies (Officials) under and responsible directly to the President.

One consideration the issuance of Presidential Decree No. 31 Year 1983 on BPKP is needed an agency or institution can perform its function freely without having the possibility of resistance to government organizational unit object inspection. Because DJPKN was Apparatus of Finance Minister, it is not possible for DJPKN to supervise and inspect the Minister of Finance and his officials indepedently.

Presidential Decree No. 31 Year 1983 shows that the Government has put BPKP organizational structure in accordance with the proportion in the constellation of government institutions that exist. BPKP the position that is independent from all the departments or agencies, of course, can better carry out its functions and objectives.

- 2001

With the change of cabinet, issued Presidential Decree No. 103 of 2001 concerning the status, duties, functions, authority, organizational structure, government institutions and non-ministerial as already amended by Presidential Decree No. 9 of 2004. Mentioned in Article 52, BPKP has the tasks of government tasks in the field of financial supervision and development according to the legislation.

General Definition and Types of Auditing

Definition of Audit

The general definition of an audit is an evaluation of a person, organization, system, process, enterprise, project or product. The term most commonly refers to audits in accounting, internal auditing, and government auditing, but similar concepts also exist in project management, quality management, water management, and energy conservation.

Organizations use first party audits to audit themselves. First party audits are used to confirm or improve the effectiveness of management systems. They're also used to declare that an organization complies with an ISO standard (this is called a self-declaration). Of course, such a declaration is credible only if first party auditors are genuinely independent and free of bias. If you decide to use first party auditors to make a self-declaration of compliance, make sure that they aren't auditing their own work.

Second party audits are external audits. They’re usually done by customers or by others on their behalf. However, they can also be done by regulators or any other external party that has a formal interest in an organization.

Third party audits are external audits as well. However, they’re performed by independent organizations such as registrars (certification bodies) or regulators.

ISO 19011 2011 also distinguishes between combined audits and joint audits. When two or more management systems of different disciplines are audited together at the

same time, it's called a combined audit; and when two or more auditing organizations cooperate to audit a single auditee organization it's called a joint audit.

ISO 19011 2011 should be used by those who carry out first and second party audits. ISO/IEC 17021 2011 should be used by those who carry out third party audits.

The Audit Process

In general, a typical audit includes the following sequential steps:

- Scheduling an opening conference to discuss the audit objectives, timing, and report format and distribution.

- Assessing the soundness of the internal controls or business systems and operations.

- Testing the internal controls to ensure proper operation.

- Discussing with management all preliminary observations.

- Discussing with management the draft audit report and their responses, if available, prior to release of the final audit report.

- Following up on critical issues raised in audit reports to determine if they have been successfully resolved.

An audit program is a set of polices and procedures that dictate how an evaluation of a business is done. This generally involves specific instructions as to what, and how much, evidence must be collected and evaluated, as well as who will collect and analyze the data and when this should be done. These types of programs are used to check up on things like a business' performance, finances, economy, and efficiency, and are generally tailored to a specific business or purpose.

Audit programs are important because they standardize the data collection and evaluation process. By setting out a specific list of steps to be followed and data to be collected, the program ensures that auditors collect all the information they need in an efficient manner while under appropriate supervision. Keeping the process standardized also means that all the data collected can be used to make useful comparisons between businesses, departments, and previous years' inspections, since the same set of data is collected each time. Additionally, having a program like this in place makes sure that any problems are discovered promptly and reported to the correct person.

Generally, there are many types of audits conducted by auditor. but broadly there are 3 main elements contained in every audit which differentiate each type of audit, namely, purpose, target, and scope. Here are some explanations of types of audits which generally conducted.

Audit based on field :

Financial statements Audit

Financial statement audit, relating to the activities of obtaining and evaluating evidence about the entity reports in order to be able to give an opinion whether the reports had been presented fairly according to the established criteria and the generally accepted accounting principle (GAAP).

Financial audits are generally performed by the company or independent public accountant who must follow accounting principles generally accepted. Many companies hire internal auditors to focus on the implementation and supervision of the company's operations to ensure compliance with organizational policies.

Performance Audit

Performance audit refers to an examination of a program, function, operation or the management systems and procedures of a governmental or non-profit entity to assess whether the entity is achieving economy, efficiency and effectiveness in the employment of available resources. The examination is objectively and systematicly done, generally using structured and professionally adopted methodologies.

In most countries, performance audits of governmental activities are carried out by the external audit bodies at federal or state level. Many of these audit bodies have established guides for conducting performance audits which explain how performance audits are planned, conducted and its results reported. Performance audits may also be conducted by Internal Auditors who are employees of the entity being audited. However, some national governments require agencies, departments and branches to periodically retain outside auditors to conduct them.

The scope of performance audits may include the detection of fraud, waste and abuse, although often these are not included in the scope. Prior to engaging in a performance audit, the auditor must have a scope and plan defined which will be used to guide the audit process.

Performance auditing differs from performance measurement, the latter being the responsibility of management of the entity. In addition, performance measurement may include a broad variety of activities that do not meet the rigour of an independent external assessment.

Management Audit

Audit management is often interpreted as the operational audit. Simple understanding of the management audit is an investigation of the organization in all aspects of management from the highest down to audit and report on the effectiveness or efficiency in terms of profitability and business activities. While simple understanding of operational audit is a systematic description of the company's activities in relation to the purpose to see, identify opportunities for improvement, or develop recommendations for improvement. Obviously both the same sense as the examination done during management operations management.

Here are some definitions according to Holmes and Overmyer (1975): "The management audit means the examination and evaluation of all information gathering functions and all phases of management functions and activities, in order to ascertain if operating are conducted in a effective and efficient manner."

Meanwhile, the American Institute of Certified Public Accountant / AICPA:

"Management audit is a systematic review of an organization's activities or of a stipulated segment of them, in relation to specified objectives for the purpose of:

• assesing performance

• identifying opportunities for improvement

• developing Recommendations for improvement

or further action "

From the definition collected above, it acquired some characteristics of management checks are:

1. Provide information on the effectiveness, efficiency and economizing operations to management.

2. Assessment of effectiveness, efficiency and economizing based on certain standards.

3. Audit directed to some or all of the operational structure of the organization.

4. These audits can be performed by accountants and non-accountants.

5. Audit results in the form of management improvement recommendations for management.

Need for Audit Management. The firm should be aware of signals that indicate the need for a management audit. Here are some of the signal:

1. Continuous decline in corporate profits and significant. Audit management tries to find the causes and solutions such as the cost is too high or the price that must be improved.

2. Turnover of Human Resources (HR) is high. This indicates inefficiency in the management of human resources, perhaps in terms of compensation or employment situation.

3. Sense of high and urgent needs of management to obtain assurance on the effectiveness, efficiency and economizing the management company including the accuracy of reports received.

4. Performance or the performance of some or all departments under the standard. The standard in question can be company regulations, company standards, industry practices and standards (ISO 9000), the principles of organization and management, as well as the principles of sound practice.

5. Acquicition Audit will admit that when acquicitioning another firm

6. Other special operational problems difficult to solve by management.

Operational Audit

An operational audit is a formal evaluation of the internal systems and procedures a company uses to produce goods or services. Made of at least four major steps, it tests how efficient and effective production operations are, which ultimately boosts revenue and profits. It also can reveal ethical issues in the business. External or internal accountants may perform the review, based on the needs of the business. This process has some disadvantages, such as potentially high cost, but it also offers advantages, such as new perspectives and increased risk awareness.

Operational audit is necessary nowadays, In general, the tools and processes a business uses to get a product or service to the public have to work as intended and be efficient. When they aren't, the company usually can't make as much money and can't be as competitive. Businesses, therefore, use these types of audits to streamline what they're doing, with the ultimate goals being to decrease waste and boost revenue and profits.

Similar to other reviews, looking at how the company is functioning overall can uncover ethical problems, such as employees using company property for personal reasons. The results of the audit let managers identify who is involved in dishonest practices, which often leads to greater accountability on the job. Companies' disciplinary and general policies often connect closely to the review for this reason.

Can be stated that the operational audit has characteristics among others the following:

· The work (productivity) will increase

· Plans, policies and other handling can be improved

· Become a healthier working atmosphere

Compliance Audit

Compliance audit, relating to the activities of obtaining and examining evidence to determine whether financial or operating activities of an entity are in accordance with the terms, specific rules, agreements, policies and applicable laws.

Compliance audit work to determine the extent of regulation, policy, law, treaty, or regulation obeyed by the entity being audited. For example, examination of individual and corporate tax returns by the tax office for compliance with the tax laws.

Testing compliance, auditors perform compliance testing that confirms the existence, effectiveness, and sustainability of the reliable operation of internal control by the organization. Compliance testing requires an understanding of the controls that will be tested, if control will be tested are the components of enterprise information systems, the auditor should consider the technology to be used by information systems. This requires an understanding of the techniques commonly used system to document information systems.

Audit Based on Audit Party

Can be stated that the operational audit has characteristics among others the following:

· Be constructive and not criticize

· Prioritizing finding fault with the auditee

· Provide early warning, do not be late

· Objective and realistic

· gradual

· Latest data, ongoing activities

· Understand the efforts of management (management oriented)

· Provide advice and not follow up on

If the operational audit going well and audit recommendations implemented by the auditee management, the benefits expected to be obtained from operational audits include:

· The costs of activities will be smaller or economically· The work (productivity) will increase

· Plans, policies and other handling can be improved

· Become a healthier working atmosphere

Compliance audit, relating to the activities of obtaining and examining evidence to determine whether financial or operating activities of an entity are in accordance with the terms, specific rules, agreements, policies and applicable laws.

Compliance audit work to determine the extent of regulation, policy, law, treaty, or regulation obeyed by the entity being audited. For example, examination of individual and corporate tax returns by the tax office for compliance with the tax laws.

Testing compliance, auditors perform compliance testing that confirms the existence, effectiveness, and sustainability of the reliable operation of internal control by the organization. Compliance testing requires an understanding of the controls that will be tested, if control will be tested are the components of enterprise information systems, the auditor should consider the technology to be used by information systems. This requires an understanding of the techniques commonly used system to document information systems.

Audit Based on Audit Party

External Auditing

External auditing is an audit conducted by public auditor hired by auditee. Staff accountants from public accounting firms who usually conduct operational audits. These professionals are not otherwise associated with the businesses they audit, so they can provide a fairly objective opinion. Stakeholders often prefer ushoing their services to internal auditors to get information because of this lack of bias, but hiring an outsider usually is more expensive.

Internal Auditing

Internal auditing is an audit conducted by internal auditor of auditee itself. In some cases, it is a better option to have someone from within the company go through the review process. Companies usually turn to internal audits when executives want a more continuous picture of what's going on in the business, sometimes going through several audits each year to stay innovative and keep revenue high. Although many employees are able to be honest and objective in an operational audit, some are not. Relying on an employee to perform the job carries the risk that the ending figures or analysis won't be entirely accurate, because an individual sometimes gets a bonus or pay increase based on how good the results are.

Internal Audit as medium to improve the effectiveness and efficiency of an organization by providing insight and recommendations based on analysis and conjecture sourced from the data and business processes. internal auditors are known as employees formed to conduct internal audits.

While the IIA'S Board of Director noted internal audit definition as follows:

"Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization Accomplish its objectives by bringing a systematic, diciplined approach to improve the effectivenenss of risk management, control's governance processes ". (1999, Vol. LVI: II pp 11; 40-41)

Internal Audit as medium to improve the effectiveness and efficiency of an organization by providing insight and recommendations based on analysis and conjecture sourced from the data and business processes. internal auditors are known as employees formed to conduct internal audits.

While the IIA'S Board of Director noted internal audit definition as follows:

"Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization Accomplish its objectives by bringing a systematic, diciplined approach to improve the effectivenenss of risk management, control's governance processes ". (1999, Vol. LVI: II pp 11; 40-41)

Subscribe to:

Comments (Atom)